Freelance platform work in the Russian Federation: 2009–2019

Abstract

At the dawn of the twenty-first century, freelance work through online platforms emerged as a new phenomenon, gradually becoming a distinctive feature of the digital economy. This paper traces the development of freelance platform work in the Russian Federation and the wider post-Soviet space. The study utilizes unique data from four online surveys conducted by the authors in 2009, 2011, 2014 and 2019 via the leading general-purpose platform for creative and knowledge-based work, FL.ru operating in the Russian language. The common methodology used to collect and analyse the data from each survey provides an opportunity to shed light on the dynamics of key indicators over the ten-year period. The study investigates socio-demographic characteristics of freelancers and their careers, motivations, working conditions and well-being, as well as the problems that freelancers encounter in their relationships with clients. Overall, the results point to the increased importance of platforms, the diffusion of the new model of work among the wider population, and the persistent informality that may hinder the future development of the online labour market. The lack of basic labour rights, collective representation and social protection is also a pressing concern.

Introduction

The development of information and communication technologies has fundamentally changed the employment landscape. Digital platforms that mediate short-term on-demand work have burgeoned. The pioneers in the digitalization of labour markets were websites dedicated to remote work, which came into existence around the turn of the millennium. In the literature, these websites are variously referred to as “online labour platforms” (Kässi and Lehdonvirta 2018; Graham, Hjorth and Lehdonvirta 2017), “crowdwork platforms” (De Stefano 2016), “freelance online marketplaces” (Aguinis and Lawal 2013; Shevchuk and Strebkov 2018) or “online labour markets” (Hong and Pavlou 2013). In this paper, we use the term “online labour markets” to describe the labour markets specifically, rather than to describe the websites themselves, for which we use the terms “online platform” and “online marketplace” interchangeably. Online labour markets represent a distinct segment of the wider gig economy, which, in contrast to localized gig work (such as taxi driving, delivery, handiwork and cleaning), implies work that can be delivered electronically. Within online labour markets, an important distinction is made between “microwork” or “piecework” platforms for low-skilled repetitive tasks (such as entering data, classifying images or transcribing texts) and freelance platforms that involve more creative and knowledge-based work by individuals such as software developers, graphic designers, writers and consultants (Berg et al. 2018). This paper explores the latter type of platform.

Although, in some cases, identifying the employment status of workers in the gig economy is problematic, in the case of online labour markets, workers typically appear as autonomous service providers referred to variously as “freelancers”, “independent contractors”, “contract professionals” or “consultants” (Cappelli and Keller 2013; Kitching and Smallbone 2012).1 Narratives about them diverge, ranging from entrepreneurial “free agents” (Malone and Laubacher 1998; Pink 2001) to precarious “logged labour” (Gandini 2019; Huws 2016). However, we still know little about the individuals who work through online platforms as freelancers, about their careers, motivations, working conditions and well-being or about the problems that they encounter in their relationships with clients. While several large-scale international surveys have addressed these questions, most reported only aggregate results for the gig economy as a whole, combining both online and local work (Berg et al. 2018; De Groen et al. 2018; Huws et al. 2019; Piasna and Drahokoupil 2019; Pesole et al. 2018). As online labour markets take on momentum, new questions arise, such as how did these characteristics evolve? In other words, what are the demographic and compositional changes in the online freelance workforce? To fill this gap, key indicators must be monitored over a period of years using a common methodology. This type of research can shed light on the dynamics and future of online platform work and can inform social and legislative initiatives.

Scholars tend to focus primarily on the global English-language platforms and on the North–South dimension of online work, virtually ignoring important developments in other parts of the world that fall outside this distinction (Kässi and Lehdonvirta 2018). However, large-scale online labour markets with millions of participants exist in other languages, reflecting the complex nature of globalization. Some evidence suggests that Chinese platforms compete with their Western counterparts in terms of the number of users (Kuek et al. 2015). The Russian language has also facilitated a large market, which includes not only citizens of the Russian Federation but also people from countries that were previously part of the former Union of Soviet Socialist Republics (USSR), as well as from anywhere where people who speak Russian actually live (Shevchuk & Strebkov, 2015). Historical roots, socio-economic and cultural context, as well as the societal impact of self-employment and platform work in these post-soviet countries, are different from other parts of the world. (Aleksynska 2021; Aleksynska, Bastrakova and Kharchenko 2018; Chepurenko 2015; Gerber 2004). The paper addresses these gaps, focusing on freelance platform work in the Russian Federation and the wider post-Soviet space. Although the literature tends to isolate platform work as a distinct phenomenon, in reality the boundaries between online and offline freelancing are permeable. We have therefore explored many issues beyond the use of platforms. The study utilizes unique data from four online surveys conducted in 2009, 2011, 2014 and 2019 via the leading general-purpose platform for creative and knowledge work, FL.ru operating in the Russian language2. The common methodology used to collect and analyse the data provides an opportunity to shed light on the key demographic and compositional changes in the online freelance workforce over the ten-year period. Conducting research on the situation of freelancers in this new context can help illuminate general traits and specific patterns of work in the online gig economy.

The rise of the digital freelance economy in the Russian Federation

1.1. The post-Soviet context of freelance work

Over the past two decades, freelance work through online platforms has emerged as a new phenomenon and has gradually become a distinctive feature of the labour market of the Russian Federation, involving not only remote work based on information and communication technologies (ICTs), but also self-employment. For several decades in the centrally planned Soviet economy, all citizens were supposed to work for state-owned enterprises, rather than for themselves. Independent work and private entrepreneurship were illegal. Only tiny niches in the areas of agriculture, construction, home care and tutoring remained in which household (but not firms) could carry out informal and part-time work to supplement their main income. In other countries, such as Hungary and Poland, which permitted limited forms of private economic activity during the shorter socialist period, entrepreneurial values and practices managed to survive and were mobilized during the market transition

The collapse of the former USSR in 1991 led to the emergence of 15 independent States with many millions of citizens who shared a common history and language but were divided by new political borders. Although dramatic political, economic and social disintegration has since occurred, the Russian language still plays an important role in the post-Soviet space. It is spoken not only in the Russian Federation but also in other post-Soviet states where many ethnic Russians live, many people speak Russian as a first language and many people learn Russian at school

1.2. Russian-language freelance platforms: An overview

The first freelance platforms in the Russian language were established in the early to mid-2000s. In 2005, FL.ru was founded, which for many years was the leading freelance platform in the region, contributing not only to creating an online infrastructure for freelancing but also to promoting a freelance culture and lifestyle. The global economic recession of 2008–2009 fostered the development of the online labour market in the Russian Federation. New business models increasingly relied on outsourcing, and more workers started to consider new employment opportunities. The number of online labour platforms increased, including those with a narrow focus on specific sectors and activities. A new economic recession also developed in the Russian Federation in 2014, manifesting notably as a dramatic currency depreciation, which meant that, for Russians, working for clients from the United States of America and Europe became particularly attractive. Various estimates suggest that both the Russian Federation and Ukraine are among the global leaders in online platform work

It is difficult to generate a precise count of workers involved in online work in the Russian Federation and elsewhere. Several dozen online labour platforms currently operate on Runet, and new platforms are constantly emerging as others lose prominence or die. These platforms differ considerably in the number of registered users, the business model used, and the scope of occupations and skills covered. Table 1.1 contains an overview of the five largest general-purpose platforms that operate in the Russian language. Two are Ukraine-based (with Freelancehunt.com operating also in the Ukrainian language). These general-purpose platforms accommodate mostly high- and medium-skilled workers across a variety of job categories (such as programming, web development, graphic design, text processing, multimedia audio processing, photography, videography, engineering, marketing and consulting). Each of the platforms (except for Freelancehunt.com) reports at least 1 million users. Two large, specialized platforms for writers also exist: Advego.com, which reports around 3 million users, and Etxt.ru, which has around 1 million users. These niche-specific platforms, focused mainly on website content creation, offer small tasks such as writing a piece of text for prices starting as low as US$0.25 for one thousand characters. With the average project price standing around US$1–2, these platforms are not among the leaders in terms of the total value of projects.

Table 1.1. The largest Russian-language freelance platforms, 2019

|

|

|

|

|

|

|

|

|---|---|---|---|---|---|---|

|

FL.ru |

Russian Federation |

2005 |

1,500 |

1,000 |

25** |

4,500** |

|

Kwork.ru |

Russian Federation |

2015 |

1,500 |

1,000 |

13.5* |

1,400* |

|

Freelancehunt.com |

Ukraine |

2005 |

700 |

510 |

12** |

850** |

|

Freelance.ru |

Russian Federation |

2010 |

1,000 |

850 |

7.5** |

520** |

|

Weblancer.net |

Ukraine |

2003 |

1,000 |

– |

4.5** |

450** |

Note: Authors’ estimations and calculations based on data from open sources:

* data reported by the website itself; – denotes data was not available.

** PrimeLance (n.d.).

On balance, five Russian-based platforms (FL.ru, Kwork.ru, Freelance.ru, Advego.com and Etxt.ru) have more than 1 million users each, totalling around 8 million users overall. The two Ukrainian-based platforms that operate in the Russian language add another 1.7 million users. It should be noted that the total number of registered users does not provide accurate information about the actual population of platform users, as individuals usually have profiles on several websites and may become inactive over time. While the figures should therefore be treated with caution, they indicate an increasing interest in online platform work in the Russian Federation.

In 2019, around 62,500 projects with a total value of US$7.7 million were published on the five general-purpose freelance platforms (FL.ru, Kwork.ru, Freelancehunt.com, Freelance.ru and Weblancer.net), with an average project price of around US$125. FL.ru accounted for around 40 per cent of all projects and around 58 per cent of their total value. The average price of a project on FL.ru was US$180. For comparison, the two largest global freelance platforms, Freelancer.com and Upwork.com, each posted five to six times more projects than FL.ru on both a daily and monthly basis. The difference in the average project price further widens the gap between the global platforms and their Russian-language counterparts, as the total value of all projects posted daily on Freelancer.com and Upwork.com is roughly two times higher than the monthly value of all projects on the five leading Russian-language platforms (PrimeLance, n.d.; Spark 2018).

Data and methodology

2.1 Methodological challenges

Compared to regular employees, the quantitative evaluation of non-standard workers poses serious methodological challenges. Freelancers belong to hard-to-survey populations (Tourangeau 2014). First, representative nationwide surveys do not provide detailed information about non-standard employment arrangements such as freelance and platform work. As platform workers generally represent only around 0.5–5.0 per cent of the adult population (Piasna 2020, 15), in dedicated representative surveys the number of respondents among platform workers is too small to study in detail their internal structure and behaviours (Piasna and Drahokoupil 2019). Instead, river samples are widely used to shed light on the characteristics of small non-demographic sub-populations, as they provide sizable samples and decrease survey costs (Lehdonvirta et al. 2021).

Second, technically, platform workers are an undefined population and a rather heterogeneous group with blurred boundaries. Individuals can engage in freelancing and platform work in a myriad of ways; some may rely on freelancing as the main source of income but show up on labour platforms quite rarely, while others may use platforms regularly but only to earn additional income or pursue a hobby. Some freelancers may stick to a particular platform, while others may be active on multiple platforms.

Third, freelancers are less accessible to researchers owing to their often-informal status and intermittent physical presence in many locations (Valenzuela et al. 2006). However, the emergence of online platforms as a new distinctive, digital-based “point of production”

Consequently, when researching freelancers, we cannot rely on the standard sociological methods based on probability sampling. We applied venue-based sampling, which is typically used to research geographically scattered populations who use certain spaces for regular meetings and congregations (Lee et al. 2014). To study populations closely related to the internet, researchers usually conduct online surveys of particular websites identified as venues for the target audience. Although some studies have used data based on transactions provided directly by the websites themselves (Hong and Pavlou 2013; Kässi and Lehdonvirta 2018; Leung 2014), this approach has limitations: website data contain a limited range of personal details and minimal socio-demographic characteristics, and they are not sufficient to generate a comprehensive description of freelancers’ work and lives.

2.2. Russian freelance survey: Ten years of research

The survey, which was in Russian, was conducted among platform workers of one of the oldest leading Russian-speaking platforms for online work based in the Russian Federation, FL.ru. The sampling assumed that, regardless of whether freelancers were registered on other similar websites, workers tended to use the largest and the most developed infrastructure for freelance contracting on the Russian-language internet. To date, four waves of this survey have been conducted (in 2009, 2011, 2014 and 2019) within the framework of the monitoring research project entitled

In the surveys, we used two filter questions to extract active freelancers from other peripheral categories, such as former freelancers, occasional freelancers and individuals who had not yet acquired a contract. These inclusionary criteria required that respondents were freelancers at the time of the survey and had accomplished more than one paid project as a freelancer within the previous year. As shown in table 2.1, the number of active freelancers varied between 2,055 and 10,574.

Table 2.1. Overview of the data collection approach and sample size, by survey wave

|

|

|

|

|

|

|||

|---|---|---|---|---|---|---|---|

|

|

|

|

|

||||

|

Active platform freelancers |

8,613 |

7,179 |

10,574 |

2,055 |

|||

|

Number of questions |

49 |

54 |

40 |

46 |

|||

|

Completion time (median), minutes |

13.9 |

12.8 |

11.1 |

11.7 |

These survey data are complemented, where necessary, by empirical data from the Russia Longitudinal Monitoring Survey – Higher School of Economics (RLMS-HSE).3 The RLMS-HSE is a series of nationally representative surveys designed to monitor the effects of reforms on the health and economic welfare of households and individuals in the Russian Federation. The 27th wave (2018) of RLMS-HSE data is used to compare the sample of platform workers.

Socio-demographic profiling

3.1. The geography of online freelance work: The Russian Federation and beyond

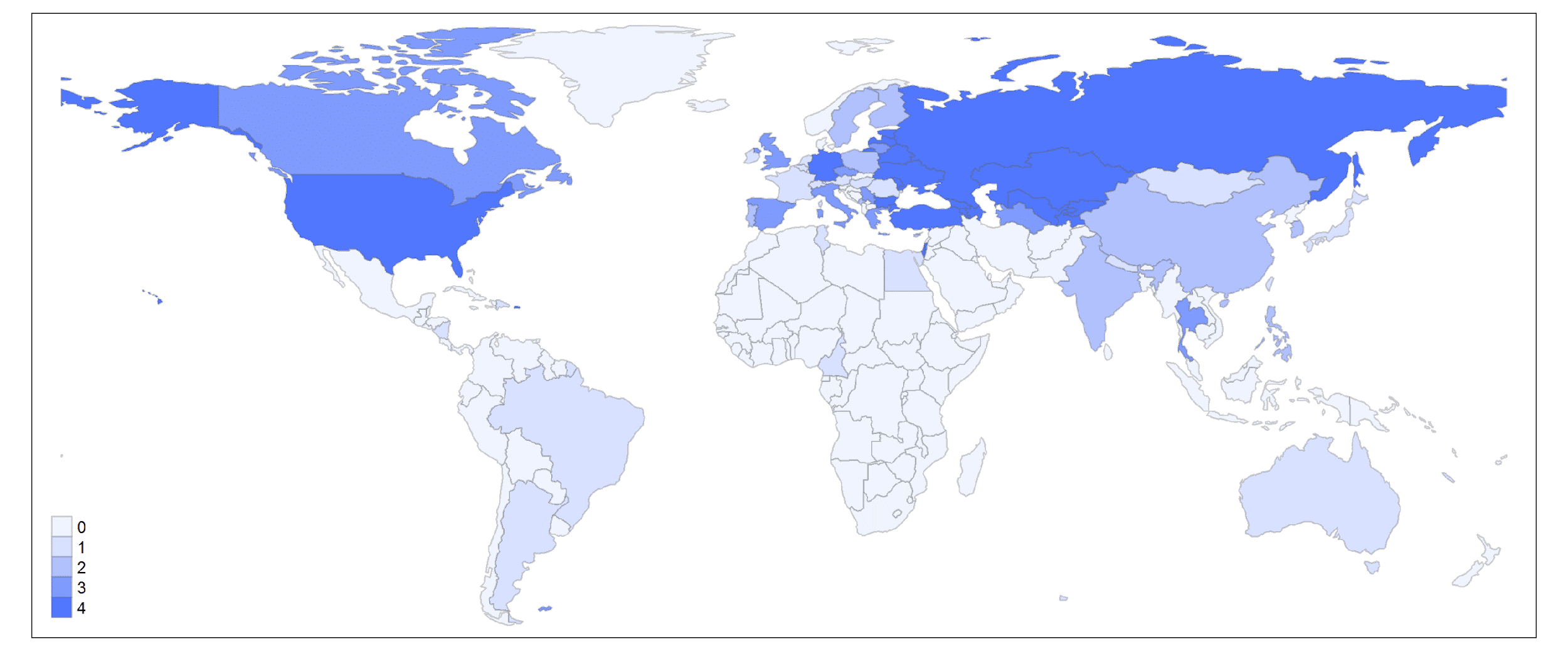

Freelancers from more than 30 countries took part in each wave of our study (between 2009 and 2019). In total, respondents from 58 countries took part across all four waves (see figure 3.1). In the 2019 survey, respondents from 37 countries participated, including 14 of the 15 former republics of the USSR (all except Lithuania), 12 European countries (Austria, Bulgaria, Czechia, Germany, Greece, Montenegro, Poland, Portugal, Romania, Serbia, Spain and the United Kingdom of Great Britain and Northern Ireland), eight Asian countries (China, India, Mongolia, Nepal, the Philippines, the Republic of Korea, Thailand and Turkey), Israel, the United States and Tunisia. The geography of the Russian-language market for remote work is much wider and is best studied using “big data” collected directly from the platform in question (Shevchuk, Strebkov and Tyulyupo 2021). It is not surprising that residents of the Russian Federation occupy more of the Russian-language freelance market (71.4 per cent) than those of other countries. They are followed by residents of Ukraine (17.0 per cent), Belarus (3.4 per cent), Kazakhstan (2.1 per cent) and the Republic of Moldova (1.1 per cent). Residents of the other republics of the former USSR together account for 2.4 per cent of the market, and another 2.1 per cent of freelancers on the Russian-language freelance market live in non-post-Soviet countries.

Figure 3.1. Geographical coverage of the four Russian-language freelance surveys (by country)

The colour indicates the number of waves of the survey in which freelancers from a given country participated.

The main trend in the geography of freelance and platform work is a gradual decentralization, reflecting the spatial diffusion of the new work model. Freelancers living outside the Russian Federation slightly strengthened their presence in the Russian-language online labour market from 24 per cent in 2009 to 29 per cent in 2019. However, these dynamics were uneven for political reasons. During the first five-year period, the share of Russian residents in the total sample decreased from 76 per cent in 2009 to 62 per cent in 2014, whereas the share of freelancers from Ukraine increased from 15 per cent to 26 per cent over the same period. However, the conflict between the Russian Federation and Ukraine that escalated in 2014 (immediately after the third wave of the survey, which ended in January 2014) reversed this emerging trend (see figure 3.2). By 2019, the share of Ukrainian freelancers had fallen to 17 per cent, and some freelancers from Ukraine had stopped working with Russian clients altogether and had left platforms based in the Russian Federation. In the same period, several Ukraine-based online platforms began to flourish (Aleksynska, Bastrakova and Kharchenko 2018). In addition, in the 2019 wave of the survey, freelancers from Crimea and Sevastopol, regions that used to be a part of Ukraine, were included in the population of Russian freelancers (1.7 per cent). Notably, the decrease in the proportion of Ukrainian freelancers in the Russian-language market occurred primarily because of the low inflow of newcomers, and not because of the outflow of more experienced freelancers. According to the 2019 survey, among respondents who became freelancers in 2013 or earlier, 23 per cent were Ukrainian, which is quite close to the result obtained in 2014 (26 per cent) and reveals only a small outflow among this group. Residents of Ukraine represented only 13 per cent of new freelancers over the five years following the conflict, however, meaning that the inflow of new users halved.

Figure 3.2. Dynamics in the geographical distribution of Russian-language freelancers, 2009–2019 (percentage)

Freelancers are widely distributed across the territory of the Russian Federation. Freelancers from 79 regions of the Russian Federation took part in the 2019 survey, and freelancers from almost all 85 regions of the Russian Federation (the only exception being Nenets Autonomous Okrug) participated in at least one of the four waves. According to the 2019 survey, 19 per cent of Russian respondents lived in Moscow and 11 per cent in St Petersburg, representing almost a third of all Russian freelancers. A significant proportion (between 1.5 per cent and 4.5 per cent) of Russian respondents were residents of the regions of Moscow, Sverdlovsk, Krasnodar, Novosibirsk, Rostov, Chelyabinsk, Voronezh, Nizhny Novgorod, Saratov, Samara, Perm, Volgograd and Tyumen. There has been a pronounced trend toward the decentralization of freelancers in the Russian Federation; between 2009 and 2019, the proportion of Moscow residents fell by almost half (from 30.6 per cent to 18.9 per cent) (see figure 3.3). Meanwhile, the proportion of freelancers from St Petersburg remained almost static (rising from 10.5 per cent in 2009 to 11.4 per cent in 2019), representing around a tenth of all Russian freelancers.

Figure 3.3. Dynamics in the geographical distribution of Russian freelancers across regions of the country, 2009–2019 (only Russian freelancers subsample, N=1261) (percentage)

Some other studies have also revealed an uneven geographical distribution in platform work. In Ukraine, four major cities together comprised 52 per cent of all online freelancers

The next important issue to consider is the client’s location. The following question was asked: “With clients from which countries and regions did you have to work during 2018?” Respondents could choose multiple options, so the sum of answers here exceeds 100 per cent. Unsurprisingly, almost all Russian-speaking freelancers (95 per cent) had worked with clients from the Russian Federation. Of them, 78 per cent had clients from Moscow, 47 per cent clients from St Petersburg and 73 per cent clients from other regions of the Russian Federation. Among the former republics of the USSR, Ukraine (26 per cent) and Belarus (15 per cent) were most often named, while the other 12 countries accounted for only 3 per cent of responses in total. Russian-speaking freelancers also actively explore global markets: one in four freelancers (25 per cent) reported having worked with a client from outside the post-Soviet space (such as Czechia, Germany, Israel, Spain, Thailand, the United Kingdom or the United States) on at least one occasion within the preceding year.

Figure 3.4 shows how a freelancer’s place of residence is connected to the country in which their clients are located. First, it is clear that the vast majority of freelancers who responded to the survey worked with clients from the Russian Federation, regardless of the country in which they lived. This rate was higher in the Russian Federation (98 per cent) and lower in the former republics of the USSR (83 per cent). While freelancers from Ukraine did carry out projects for local clients (71 per cent), they very often also worked with clients from the Russian Federation (89 per cent). The same applies to Belarusian freelancers: although the proportion of respondents who had completed local projects was rather high (66 per cent), it did not surpass the proportion who had worked with clients from the Russian Federation (85 per cent).

The situation of clients from non-post-Soviet countries is interesting. Naturally, such clients tend to assign projects to residents of their own countries (65 per cent). However, Ukrainian freelancers are actively cultivating this market (39 per cent reported having worked with clients from a non-post-Soviet country), whereas it remains largely unexplored by residents of the Russian Federation (21 per cent). As the Russian Federation has a large domestic market, Russian freelancers seemingly have enough work from local clients and therefore do not need to enter the international market.

Figure 3.4. Clients’ location for Russian-speaking freelancers from different countries, 2019 (percentage)

Freelancers from the Russian Federation also have geographically localized relationships with clients (see figure 3.5). Despite the global nature of remote job markets and the ability to find clients anywhere, 94 per cent of Moscow residents reported that, in 2018, they had worked with companies and individuals from Moscow, and 86 per cent of St Petersburg residents reported working with clients in St Petersburg. Residents of other regions of the Russian Federation, meanwhile, collaborated primarily with clients from other regions (84 per cent). Despite all the numerous opportunities for remote work provided by the internet, territorial proximity between the client and the contractor is still an important factor. In line with previous research, we found some tendency to favour geographically proximate transactions (Graham, Hjorth and Lehdonvirta 2017; Hong and Pavlou 2013). In the study based on “big data”, this tendency was found to differ depending on the freelancer’s occupation, thereby illuminating the spatial division of online labour (Shevchuk, Strebkov and Tyulyupo, forthcoming). However, many freelancers looking for work go far beyond their city or region: 83 per cent of St Petersburg residents and 77 per cent of residents from other Russian regions worked for clients from Moscow, while 33 per cent of Moscow residents and 46 per cent of residents of other Russian regions found clients in St Petersburg.

Figure 3.5. Clients’ location for Russian freelancers from different regions, 2019 (only Russian freelancers subsample, N=1261) (percentage)

3.2. Basic demographics

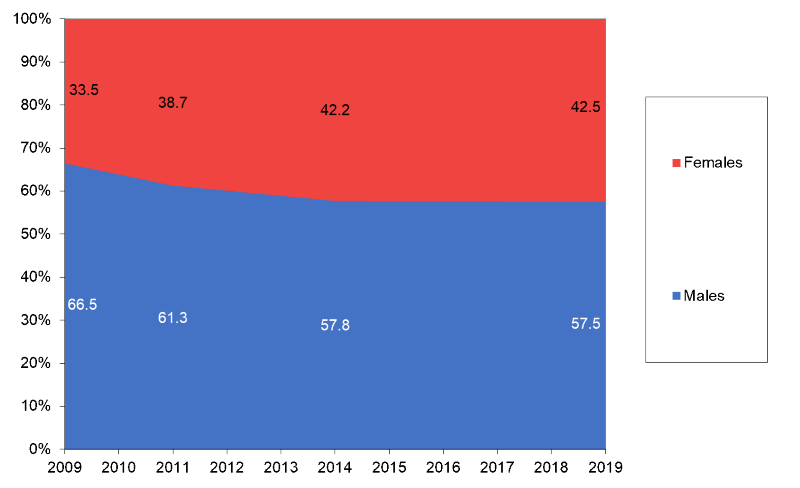

Many studies have shown that online freelancers and platform workers are, in general, somewhat more likely to be male than female, although the gender profile varies by country and by platform (Aleksynska 2021; Huws et al. 2019; Kuek et al. 2015; Pesole et al. 2018; Berg et al. 2018). Our surveys not only support these results but also shed light on the evolution of the gender composition of the online freelancer population over time. While the gender disparity was particularly pronounced at the time when online work was just emerging, a gradual alignment of the gender structure has taken place. As shown in figure 3.6, the proportion of women generally increased throughout the study period: in 2009, around two thirds of active freelancers were male and 33 per cent were female, but by 2014 the gap had narrowed, with 58 per cent of freelancers identifying as male and 42 per cent female. Over the next five years, the situation stabilized; in 2019, the proportion of women was the same as in 2014 (42 per cent). Men therefore seem to have pioneered the development of online markets, but, as this kind of work became more generalized, women also started taking up online work more actively, and the online market progressively started to resemble the general labour market.

Figure 3.6. Dynamics in gender distribution among Russian-language freelancers, 2009–2019 (percentage)

The same dynamics can also be partially seen when looking at the proportion of men and women based on their experience, or “tenure”, of freelance work (see figure 3.7). In 2019, among newcomers (those who had started working as a freelancer, or as a platform worker, within the preceding year), the proportion of women was higher than among more experienced workers; in fact, women outnumbered men, accounting for 56 per cent of all newcomers. Moreover, comparisons with earlier waves of the survey indicate that there was no significant outflow of women from the freelancer population over time: in 2019, among workers with more than five years of online tenure, the proportion of women remained almost the same as that observed in 2014 (37 per cent versus 42 per cent). Given this, there are good reasons to believe that the share of women in the online freelance market will continue to grow.

Figure 3.7. Gender distribution by freelance tenure, 2019 (percentage)

In 2019, the overall gender balance remained uneven among freelancers based in Ukraine, Belarus and other countries of the former USSR, with many more men than women (68 per cent versus 32 per cent) engaged in freelance work. In the Russian Federation and non-post-Soviet countries, the proportion of female freelancers was much higher (around 45 per cent).

Most freelancers tend to be quite young. In 2019, around half of respondents were under the age of 32 years and only a fifth were aged over 40. Studies conducted in advanced market economies with long-standing freelance traditions report very different age patterns for the freelance population, with an average age of around 45 years (Rodgers, Horowitz and Wuolo 2014), although online freelancers may be somewhat younger on average (Piasna and Drahokoupil 2019). Typically, contracting is “not a young person’s game” (Barley and Kunda 2004, 53), but rather the “free agent” option of an experienced worker. We propose that, in the Russian Federation, younger generations are not only more advanced with regard to ICT usage, but they also socialize during the post-Soviet period and are more open to independent and entrepreneurial work. The study of online freelancers in Ukraine (another post-Soviet country) revealed an almost identical age distribution; the average age was 33, and only 21 per cent of freelancers were older than 40 (Aleksynska, Bastrakova and Kharchenko 2018).

The average age of Russian-language freelancers has experienced a clear upward trend, increasing from 26.6 years in 2009, to 28.5 years in 2011, to 31.5 years in 2014 and finally to 33.5 years in 2019. In particular, the percentage of freelancers aged over 30 more than doubled, from 22 per cent in 2009 to 54 per cent in 2019 (see figure 3.8).

Figure 3.8. Age distribution, 2009 and 2019 (percentage)

This upward trend was not only due to the natural “ageing” of the website’s audience year by year, but also a result of a growing proportion of more mature workers among newcomers (see figure 3.9). We anticipate that this trend will continue in future.

Figure 3.9. Age distribution of newcomers (freelancers with tenure of less than 1 year), 2009–2019 (percentage)

In 2009, some significant gender differences in age distribution were observed. The average age was around 26 years for male freelancers and 28 years for female freelancers. Among men, 36 per cent were classified as young (under 22 years old), while this proportion was much lower for women (22 per cent). By 2019, however, these differences had disappeared (see figure 3.10).

Figure 3.10. Age distribution by gender, 2009 and 2019 (percentage)

In 2019, the average age of freelancers differed from country to country. Ukrainian workers were generally younger, with an average age of 32 years, compared with workers from the Russian Federation and other countries of the former USSR, who had an average age of 34 years. Freelancers from non-post-Soviet countries were the most mature, with an average age of 38 years. Workers over 40 years of age represented 14 per cent of all freelancers in Ukraine, 22 per cent in the Russian Federation, 25 per cent in other countries of the former USSR and 34 per cent in non-post-Soviet countries.

Despite conventional wisdom, studies suggest that online freelancers and platform workers are, in general, likely to have a family and children (Aleksynska, Bastrakova and Kharchenko 2018; Pesole et al. 2018). This suggests that, despite the general insecurity, freelancing may be an attractive option for those who need more flexibility to balance work and family. In 2019, almost half of respondents were married (46 per cent) at the time of the survey, 17 per cent lived with a partner and 37 per cent had never been married, were divorced or were widowed. There were no significant differences in marital status by gender. Ten years earlier, in 2009, freelancers were, on average, younger; the proportion of married workers was therefore much lower (32 per cent) and the proportion of single workers was much higher (47 per cent) (see figure 3.11).

Figure 3.11. Dynamics in family status among Russian-language freelancers, 2009–2019 (percentage)

In 2019, 40 per cent of freelance workers had children younger than 16 years old in their household: 26 per cent had one child, 11 per cent had two children and 3 per cent had three or more children. The remaining 60 per cent of respondents lived in a household without children. Ten years earlier, in 2009, only one third of households (32 per cent) had children younger than 16 years old: 25 per cent had one child, 6 per cent had two children and 1 per cent had three or more children. We conclude that, after very young freelancers pioneered the online labour market, more mature individuals with greater family obligations increasingly turned to freelance and platform work in the Russian Federation.

Russian legislation guarantees female and male caregivers the right to return to their jobs after parental leave (which can be extended up to 36 months). A caregiver can combine parental leave with a part-time freelance job. The State provides moderate financial support for caregivers and households with many children through various mechanisms. Around 6 per cent of freelancers (12 per cent of females and 2 per cent of males) used this opportunity to care for a child under the age of three. This figure did not change significantly over the ten-year study period, remaining in the range of 5 to 7 per cent.

3.3. Education, occupation and skills

Russian-language freelancers are very well educated. In 2019, 80 per cent had some post-secondary education and 67 per cent held a university degree; of these, 16 per cent held a bachelor’s degree, 33 per cent held a specialist degree (a five-year education programme very popular in the Russian Federation until the end of the 2000s) and 16 per cent held a master’s degree. Furthermore, around 2 per cent of freelancers held a “Candidate of Sciences” or “Doctor of Sciences” degree (equivalent to a PhD). A tenth of respondents were young and were still studying at the time of the survey (2 per cent at high school and 8 per cent at university). By comparison, around 30 per cent of all Russian workers hold a university degree.

Since 2009, the level of education among freelancers has increased dramatically; the proportion of survey respondents without a university degree (but with secondary education or unfinished higher education) declined from 46 per cent in 2009 to 30 per cent in 2014 (rising only slightly to 33 per cent in 2014) (see figure 3.12). As noted above, the Russian-language online labour market was pioneered by very young freelancers, who were later followed by more mature and educated workers.

Figure 3.12. Dynamics in educational level among Russian-language freelancers, 2009–2019 (percentage)

The education level among female freelancers is quite high; 73 per cent of female freelancers have a bachelor’s degree or higher, compared with 63 per cent of male freelancers. Female freelancers are, therefore, generally more educated than their male counterparts. The most educated Russian-speaking freelancers live in non-post-Soviet countries: 74 per cent hold a university degree and 34 per cent hold a master’s degrees, MBA or PhD. Freelancers from Ukraine are also well educated: 72 per cent hold a university degree and 26 per cent hold a master’s degree, MBA or PhD.

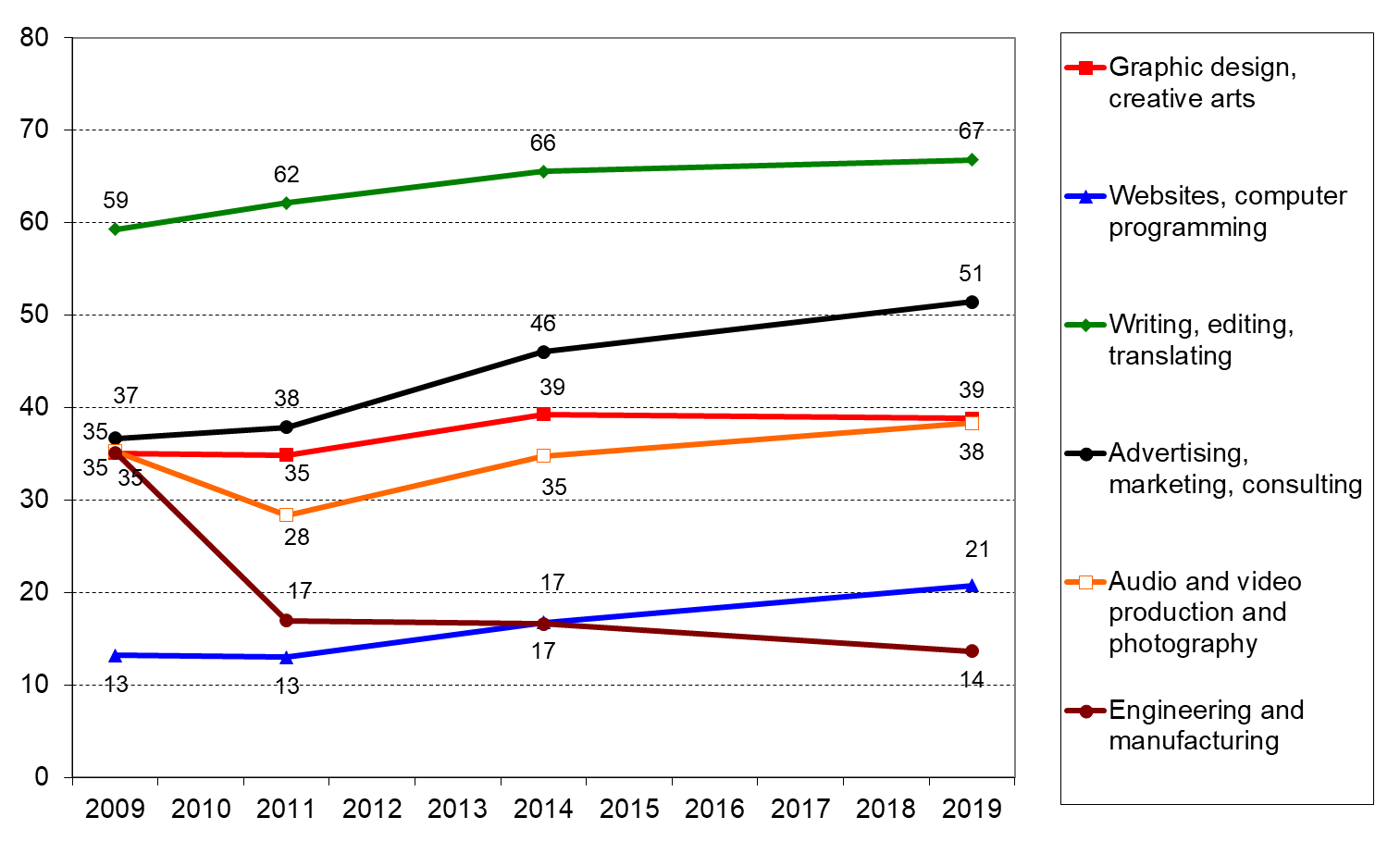

Online labour platforms arrange jobs and freelancers’ skills into categories that represent conventionally recognized divisions of tasks (Leung 2014). The scope of the skills covered is relatively limited and varies little around the world, although the particular occupational structure may differ across various websites. The basic prerequisite for remote work is that the results can be produced in digital format and transmitted via the internet. Unsurprisingly, programmers, website builders and other ICT professionals were the pioneers of online labour markets. According to the surveys that we conducted, the main areas of Runet freelancer expertise include graphic design and creative arts (37 per cent); websites, computer programming and other IT jobs (29 per cent); writing, copywriting, editing and translating (28 per cent); advertising, marketing and consulting (20 per cent); audio and video production and photography (14 per cent); and engineering (8 per cent). As multiple answers were possible, the sum of all answers exceeds 100 per cent.

We observed a trend of increasing occupational diversification. Changes in the general occupational structure of the online labour market are leading to a rising supply of skills that were previously under-represented. Since 2009, the market share of two particular skill categories has grown steadily: engineering (from 2 per cent to 8 per cent) and business services, such as advertising, marketing and consulting (from 11 per cent to 20 per cent) (see figure 3.13). The proportion of freelancers with expertise in text-based jobs (writing, copywriting, editing, and translating) increased from 21 per cent in 2009 to 33 per cent in 2011 and then dropped again to 28 per cent in 2019. Among the professional skills, the most significant decline in market share was observed for IT jobs (such as website development and computer programming), which dropped from 42 per cent in 2009 to 29 per cent in 2019. The market share of the graphic design and creative arts sectors also decreased, albeit less dramatically, from 44 per cent in 2009 to 37 per cent in 2019. We conclude that, not only have ICT workers increasingly joined the online labour market, but so have freelancers from other occupational groups, having become familiar with freelance platform work.

Figure 3.13. Dynamics in professional skills among Russian-language freelancers, 2009–2019 (percentage)

In addition to noting the growing proportion of women freelancers, important differences were observed in the type of work that women and men do online as freelancers. There is strong gender segregation in the tasks performed: men dominate the IT sector, including programming and website development (79 per cent of IT workers are male) and engineering (86 per cent of workers are men); in contrast, women are largely over-represented in text-based work (where 67 per cent of workers are women). In fact, copywriting, editing and translating are the only sectors where the proportion of women was higher than the proportion of men throughout all ten years of the study (see figure 3.14). Looking at all four waves of empirical data, we can see a particularly rapid and dramatic growth in the proportion of female online freelancers in the IT sector (from 13 per cent to 21 per cent), business services (from 37 per cent to 51 per cent) and text-based services (from 59 per cent to 67 per cent). The three other occupations covered by the survey did not witness a significant growth in the proportion of female freelancers.

Figure 3.14. Proportion of women in different categories among Russian-language freelancers, 2009-2019 (percentage)

The survey revealed the differences in the distribution of professional skills between countries (see figure 3.15). While freelancers from the Russian Federation are under-represented in the IT sector, they represent a rather high proportion of workers in the business services sector (such as advertising, marketing and consulting) and in multimedia (such as audio and video production and photography). Ukrainians hold a strong position in the design and creative arts sectors, and a moderate position in the IT and text-based sectors. Workers from the other countries of the former USSR tended to specialize in design, creative arts and multimedia (audio and video production and photography). Meanwhile, Russian-speaking freelancers living in non-post-Soviet countries were leaders in the business service sector and in the text-based sector, primarily translation, as they were likely to have good foreign language skills as a result of living abroad.

Figure 3.15. Distribution of professional skills by freelancer’s country of residence, 2019 (percentage)

Among freelancers living in the Russian Federation, 63 per cent of respondents had received paid work over the preceding year only from clients who also lived in the Russian Federation. One in three Russian freelancers (35 per cent) collaborated both with Russian clients and with clients living abroad, and only a very small fraction of Russian freelancers (2 per cent) had connections only with clients living outside the Russian Federation. The professional skill profiles of these groups differed, demonstrating a slight task segregation according to the market served (see figure 3.16). Almost half of workers who specialized in the IT sector (46 per cent) had at least some clients living abroad, while workers in the engineering and business service sectors focused primarily on the domestic market and had only rare connections with foreign clients.

Figure 3.16. Market served by professional skill, 2019 (only Russian freelancers subsample, N=1261) (percentage)

While formal education may play an important role in the human capital formation of freelance professionals (Shevchuk, Strebkov and Davis 2015), in order to be continually employable freelancers often span traditional functions and occupational boundaries in response to changes in market demand. The literature has shown how contract workers make calculated efforts to manage their career progression by developing skills in new areas through the “learning by doing” process (Barley and Kunda 2004; Osnowitz 2010). Although freelance contracting is based around professional expertise, freelancers often take on projects beyond their field of study or even their prior working experience. In developed economies, significant concerns regarding vertical skill mismatch and deskilling have arisen as highly educated people have been forced to turn to simple tasks in the gig economy in the absence of decent work opportunities in the traditional labour market (Pesole et al. 2018). A subjective assessment of horizontal educational mismatch was conducted based on responses to the question: “Does the work you do as a freelancer match the subject area that you studied after high school?” Responses were provided on a four-point Likert scale, ranging from “fully matches” to “fully mismatches”.

The extent of mismatch in our sample is higher than that previously reported in the literature. We found that most Russian-language freelancers work in an area that is absolutely (36 per cent) or mostly (19 per cent) unrelated to their field of study. Although horizontal educational mismatch is an important factor in the Russian-language freelance market (Shevchuk, Strebkov and Davis 2015), it does not diverge greatly from the trends seen in the general labour market of the Russian Federation, where 38 per cent of all Russian workers with a university education experienced mismatch in 2017. The trends in education and educational mismatch deserve deeper analysis and may be rooted in general structural problems in the economy of the Russian Federation.

Horizontal educational mismatch is more common among male freelancers than female freelancers: 38 per cent of men versus only 33 per cent of women consider their work to be fully mismatched with their area of university education. The highest level of severe mismatch can be observed among workers with an incomplete higher education or a bachelor’s degree (40 per cent).

A person is typically not expected to have a diploma in order to take on the majority of the work tasks offered online, such as website building, mobile application development, logo design, blog writing or online advertising consulting. However, for engineering and building architecture, credentials are more important, and legal practice requires formal certification. Indeed, according to the 2019 survey data, horizontal educational mismatch is more widespread among creative occupations, such as multimedia (audio/video/photography), graphic design and arts, website development and writing/editing (see figure 3.17). There are considerable differences between the two types of IT work (website development and programming) and the two types of text work (writing/editing and translating); for programming and translating, education requirements are stronger, whereas for website development and writing/editing they are much weaker.

Figure 3.17. Horizontal educational mismatch by professional skill, 2019 (percentage)

Freelance careers and platform work

4.1. Motivation

Although many structural factors affect labour market behaviour, personal preferences – such as values – are an important influence. Work values encompass the relative importance that an individual places on various aspects of work, including work settings and work-related outcomes (Kalleberg 1977). Work values refer to what an individual wants out of work in general, rather than to the characteristics of a particular job.

Work values were measured through a multiple-choice question, identical to that used in the World Values Survey: “Which of the following do you personally think are the most important aspects in a job?” Respondents were urged to choose from among 12 items that covered a wide range of job characteristics: “good pay”, “not too much pressure”, “good job security”, “a job respected by people in general”, “good hours”, “an opportunity to show initiative”, “generous vacation time”, “a job in which one feels able to achieve something”, “a job that is interesting and creative”, “a responsible job”, “a job that meets one’s abilities”, and “an opportunity to acquire new knowledge and skills”.

The three most important values for Russian-language freelancers were good hours (72 per cent), an interesting and creative job (70 per cent) and good pay (67 per cent) (see figure 4.1). Following them in importance were the opportunity to acquire new knowledge and skills (62 per cent) and the opportunity to use one’s abilities (61 per cent). Freelancers were not inclined to minimize their work effort, placing least focus on generous vacation time (10 per cent), minimum pressure at work (17 per cent) and having a respected (19 per cent) or responsible (21 per cent) job. Job security was also of little significance to them (23 per cent). This structure of freelancers’ work values remained almost unchanged over the whole ten-year period in which the surveys were conducted.4 Nevertheless, the frequency of two characteristics did grow significantly: more freelancers began to appreciate good hours (from 60 per cent to 72 per cent) and an opportunity to use one’s abilities (from 33 per cent to 61 per cent). In turn, respondents became less likely to mention good pay (from 80 per cent to 67 per cent), job security (from 34 per cent to 23 per cent) and an interesting and creative job (from 82 per cent to 70 per cent). These changes are most likely associated with the transformations seen in the structure of the freelance population over the ten-year period, during which the population became more mature and the proportion of respondents for whom freelance work was the main or only source of income increased.

Figure 4.1. Work values of Russian-language freelancers, 2019 (percentage)

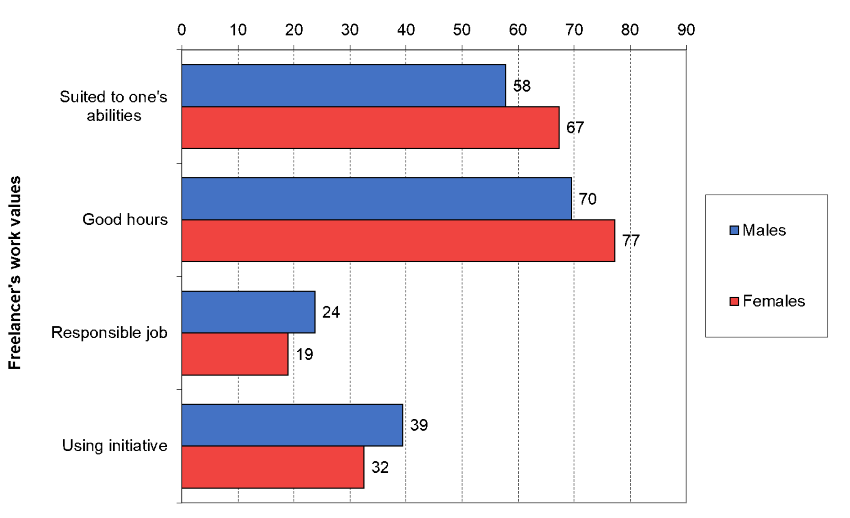

Slight differences were observed in the structure of work values between male and female freelancers (see figure 4.2). The desire for opportunities to show initiative and the desire to perform a responsible job were more common among men, while women were more attracted to good hours and to jobs that suited their abilities.

Figure 4.2. Key gender differences in freelancers’ work values, 2019 (percentage)

The importance of some work values changed significantly with age (see figure 4.3). While young freelancers were most attracted to good pay, low-pressure work, and opportunities to acquire new knowledge and skills, show initiative or achieve something, older workers reported being more drawn to jobs that were generally respected and that suited their abilities.

Figure 4.3. Key age differences in freelancers’ work values, 2019 (percentage)

One of the most intriguing issues is why individuals become freelancers. The entry into self-employment is usually discussed in terms of “pull” and “push” factors. In the Russian Federation – and in many developing countries – self-employment is driven by poor job prospects and the need to survive. The vision of self-employment as an entirely necessity-based activity is not true in the case of freelancers, however. In 2019, a large proportion of respondents stated that they had started freelancing because they needed to make extra earnings (38 per cent); others, meanwhile, reported that the driving factor was that they had been fired (15 per cent) or were obliged to look after small children (8 per cent) (see figure 4.4). Around 30 per cent of freelancers reported these push factors exclusively. At the same time, however, more than half of freelancers (53 per cent) reported being driven mainly by pull factors, as they had turned an activity that used to be a hobby into a job (32 per cent), they were seeking a new professional experience (16 per cent) or they no longer wanted to be an employee (45 per cent). For these freelancers, becoming an independent contractor was largely a matter of personal choice. The rest of the respondents (17 per cent) had mixed incentives, combining push and pull factors.

Figure 4.4. Reasons to become a freelancer, 2019 (percentage)

Men were much more likely than women to become freelancers through turning a hobby into a job (37 per cent versus 26 per cent), while women were, unsurprisingly, much more likely to choose freelance work once they had had a small child (17 per cent versus 1 per cent).

All three pull factors were cited more often by young freelancers under the age of 30 than older freelancers: 50 per cent of respondents under 30 years old were driven by the desire to no longer be an employee versus only 38 per cent of respondents over the age of 40. Conversely, the proportion of respondents over the age of 40 who had become freelancers owing to a dismissal and the subsequent inability to find other employment was almost twice as high as that of respondents under 30 years old (21 per cent versus 11 per cent).

4.2. Divergent careers

Russian-language freelancers have limited work experience and a short freelancer tenure, as they are a relatively young cohort. Most respondents had worked for three years or less as a freelancer, although this proportion declined from 77 per cent in 2009 to 51 per cent in 2019 (see figure 4.5). The average freelance tenure increased almost twofold over the same period, from 2.5 years in 2009 to 4.8 years in 2019, and the proportion of highly experienced workers with ten or more years of freelance experience increased from 4 per cent in 2009 to 15 per cent in 2019. In advanced market economies, individuals tend to have a much higher level of freelance experience; for instance, Rodgers, Horowitz and Wuolo (2014, 715) reported that independent workers in the United States had, on average, around ten years of tenure as a “free agent”. However, we can conclude that online freelancing in the Russian Federation is becoming more of a long-term career choice.

Figure 4.5. Dynamics in length of freelance tenure held, 2009–2019 (percentage)

In 2019, the most experienced Russian-language online workers lived in Ukraine and non-post-Soviet countries, where the average freelance tenure was 5.6 years and 6.5 years respectively. In the Russian Federation, meanwhile, it was 4.5 years. On average, men had more experience as freelancers than women (5.4 years of tenure versus 4 years of tenure).

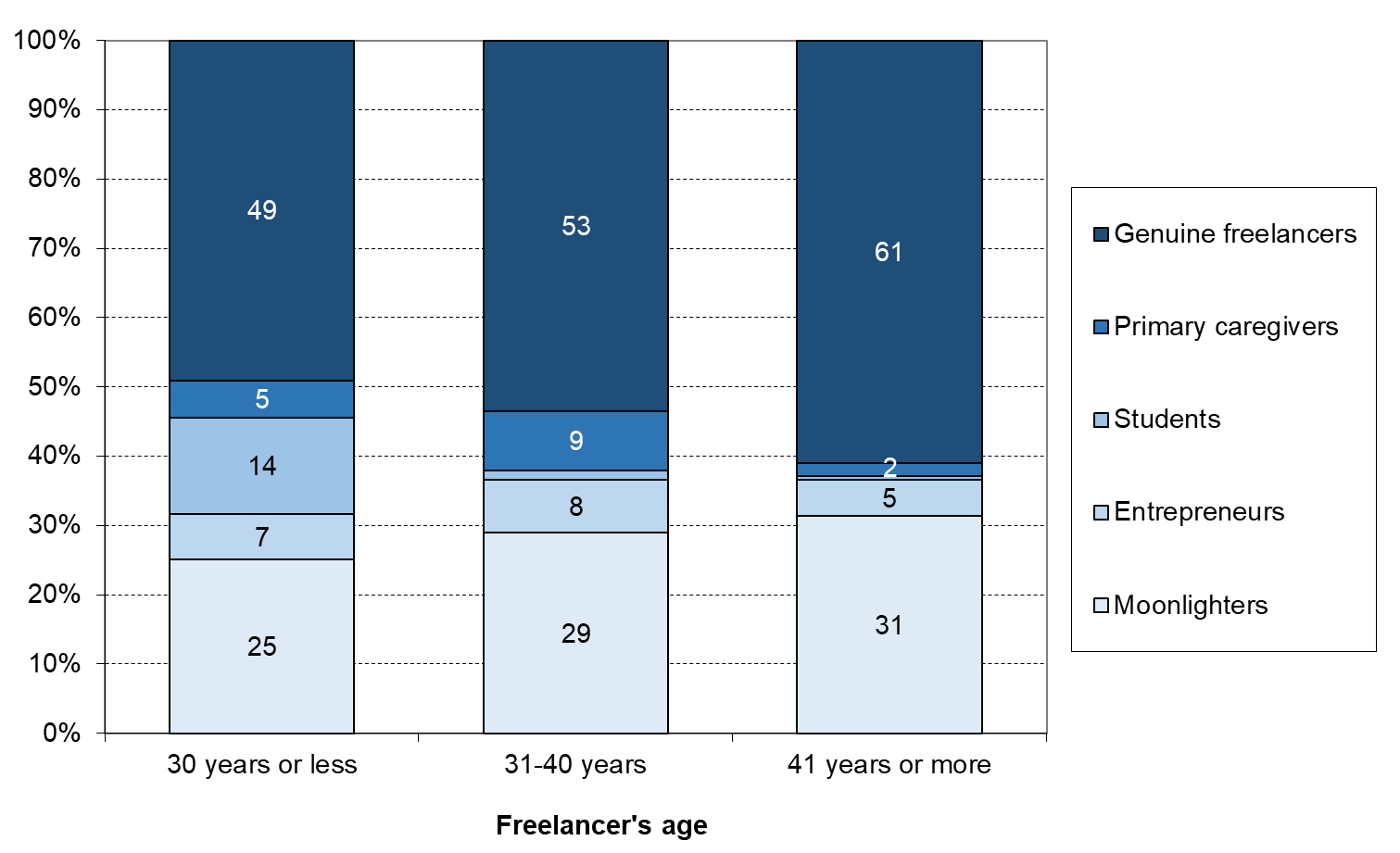

There is convincing evidence that many freelancers become involved in the gig economy on a part-time basis to earn additional income or to experiment with new work patterns (Berg 2016; Huws et al. 2017; Piasna and Drahokoupil 2019). To unravel the complexity of freelancer employment situations, we applied the concept of a portfolio career as proposed by Handy (1989), which incorporates both paid and unpaid activities. This approach provides a more comprehensive view of the role of freelancing in workers’ lives. Besides “genuine freelancers”, who are primarily own-account workers, we examined “hybrid self-employment” (Bögenhold 2018), in which an individual simultaneously holds two jobs of different employment types. We used five different principal employment situations to distinguish between freelancers. For genuine freelancers, independent contracting is a full-time activity and the only source of income. For “moonlighters”, freelancing is a second job that complements a conventional employment contract. Parallel entrepreneurs start up and manage small businesses with hired employees while remaining engaged as freelance workers. Freelancing is also a typical source of income for students and for individuals with primary caregiver responsibilities.

In the Russian-language context, freelancing tends to be a second job for many individuals, although there was a huge decrease in moonlighters over the study period, from 45 per cent in 2009 to 27 per cent in 2019 (see figure 4.6). The proportion of genuine freelancers in our sample showed a steady upward trend, increasing from 22 per cent in 2009, to 29 per cent in 2011, to 34 per cent in 2014 and finally to 52 per cent in 2019. As older and more experienced workers have recently commenced freelancing, the percentage of students among the freelance population decreased dramatically during the study period, dropping from 18 per cent in 2009 to 8 per cent in both 2014 and 2019. The proportion of entrepreneurs and caregivers remained mostly stable during the study period (7 per cent and 6 per cent respectively in 2019). We can therefore conclude that more and more people in the Russian Federation are approaching freelancing as a viable labour market option.

Figure 4.6. Dynamics in freelancer employment status, 2009–2019 (percentage)

Women are much more likely than men to combine freelance work with caring for children under 3 years old (10 per cent versus 2 per cent). In Russian legislation, employees are entitled to care for a young child while holding on to their jobs. Due primarily to this imbalance, women are slightly under-represented among genuine freelancers (51 per cent women versus 54 per cent men), moonlighters (25 per cent versus 29 per cent) and entrepreneurs (5 per cent versus 8 per cent).

Relatively young freelancers under 30 years old are much more likely to still be studying at school or university (14 per cent); almost no freelancers over 30 years old reported that they were still in education. This difference is likely the cause of the lower proportion of genuine freelancers and moonlighters among young persons (see figure 4.7). The proportion of entrepreneurs does not vary significantly according to age.

Figure 4.7. Freelancer employment status by age group, 2019 (percentage)

Moonlighting is more common in countries of the former USSR (except for the Russian Federation and Ukraine), with 38 per cent of respondents combining freelance activity with employed work. In the Russian Federation and Ukraine, this figure is much lower at 28 per cent and 20 per cent respectively. Ukraine has the highest proportion of genuine freelancers (65 per cent). The proportions of entrepreneurs, students and caregivers are approximately the same everywhere.

Across professional skills, engineering specialists are very different to all others; more than half are moonlighters (52 per cent), and 38 per cent are genuine freelancers. In contrast, the graphic design sector has the lowest level of moonlighters (22 per cent) and the highest level of genuine freelancers (55 per cent). The proportion of entrepreneurs is the highest (10 per cent) among workers with expertise in website development, computer programming and other IT jobs, as well as among specialists in business services (such as advertising, marketing and consulting).

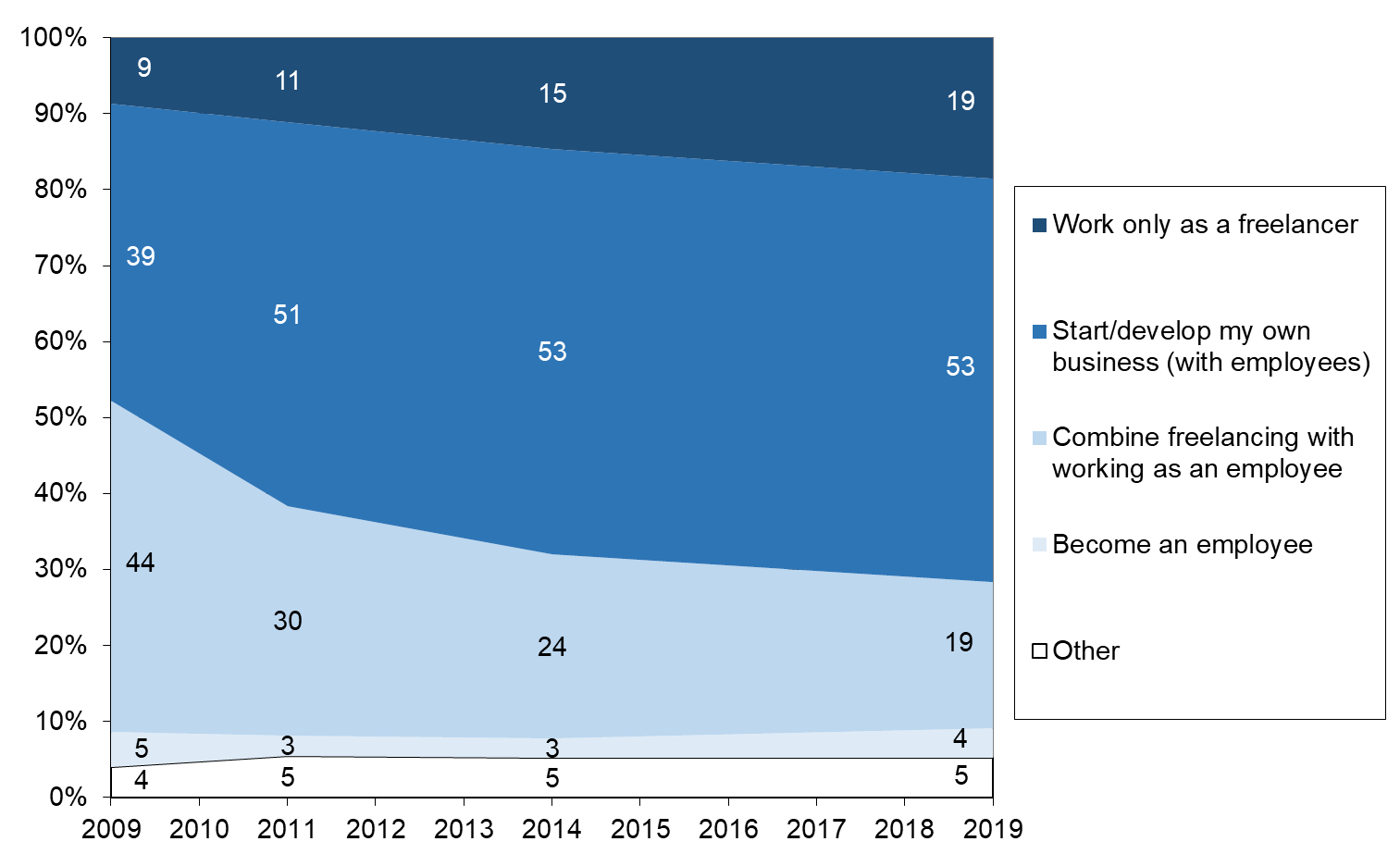

To explore career intentions, we asked freelancers what they planned to do in the next five years of their working life. Our findings showed that a very small number of respondents (4–5 per cent) intend to leave freelancing for a standard job within the next five years (see figure 4.8). In 2019, one fifth of respondents stated that they would prefer to be a moonlighter in future, and the same proportion (19 per cent) planned to become a genuine freelancer. This proportion had increased substantially over recent years, up from only 9 per cent in 2009. One particularly noteworthy finding, which illuminates the entrepreneurial orientation of current freelancers, was that 17 per cent planned to leave freelancing to manage a small business with employees, and a further 36 per cent wanted to combine freelancing with entrepreneurship. Generally, freelancers establish small firms in their area of expertise, such as software companies, design studios or advertising agencies. Although not all career intentions may be realized, these findings show some support for the prospect of freelancing as a path to entrepreneurship (Shevchuk and Strebkov 2017).

Figure 4.8. Dynamics in freelancers’ career intentions, 2009–2019 (percentage)

4.3. Beyond platforms

The literature has raised concerns about the transformative role of labour platforms tending to ignore the working lives of freelancers beyond those platforms. This may be misleading and may oversimplify the reality of freelance and platform work. Our surveys help to shed light on “platformization” as a gradual process of increasing influence and importance of online labour platforms in the Russian Federation. Our respondents tended to use multiple online platforms, including English-speaking platforms; the proportion of freelancers registered on two or more platforms grew from 50.6 per cent in 2009 to 66.4 per cent in 2019, and the proportion of freelancers registered on a English-speaking platform grew from 9.6 per cent to 30.5 per cent over the same period.

Although matching freelancers to clients is a principal function of online labour platforms, in real life freelancers may obtain job projects from various sources. Online platforms (freelance marketplaces) are the main source of jobs for Russian-language freelancers; overall, two thirds (67 per cent) of respondents in the 2019 survey regularly used platforms as job search channels. However, only 14 per cent used platforms as the only source of work, and most respondents (53 per cent) combined platforms with other sources (such as regular clients, referrals or social media). Over the study period, the importance of platforms increased from year to year (see figure 4.9). In 2009, only 42 per cent of freelancers used platforms to search for jobs, and 8 per cent considered platforms to be their only source of work, meaning that they relied exclusively on an open market.

Figure 4.9. Dynamics in the use of online freelance platforms as job search channels, 2009–2019 (percentage)

At the same time, our data show that freelancers often obtain jobs not from the anonymous market, but rather from persons known to them (see figure 4.10), such as regular clients (65 per cent), referrals from former clients (49 per cent), friends and acquaintances (28 per cent) and other freelancers and colleagues (18 per cent). Among the respondents, 80 per cent relied on their social capital to some degree, and 24 per cent reported relying entirely on their social capital, meaning that they found jobs exclusively through established social ties.

The very idea of an online platform is to bring together spatially dispersed buyers and sellers of remote services. Theoretically, this online infrastructure is supposed to facilitate arm’s length ties and favour the global spot market. However, our data have provided a more nuanced image of a socially embedded freelancer, rather than an atomized platform worker. More research is needed on this in other contexts (Wood et al. 2019; Shevchuk and Strebkov 2018).

Figure 4.10. Channels for obtaining job projects, 2019 (percentage)

The data reveal that, during their freelance careers, workers accumulate social capital, represented by regular clients and referrals (see figure 4.11). Freelancers who are just starting as platform workers (with tenure of less than one year) rarely use regular clients and referrals to obtain jobs (39 per cent for regular clients and 38 per cent for referrals). The greater the experience and tenure of freelancers, the more often they use their social capital. Among respondents with a freelance tenure of more than nine years, 82 per cent worked with regular clients and 72 per cent used referrals.

Figure 4.11. Channels for obtaining job projects by freelance tenure, 2019 (percentage)

As a result, the proportion of freelancers who relied exclusively on online platforms rapidly decreased with each year of freelance tenure, from 30 per cent among “beginners” to 5 per cent among “veterans” (see figure 4.12).

Figure 4.12. Obtaining job projects via online platforms by freelance tenure, 2019 (percentages)

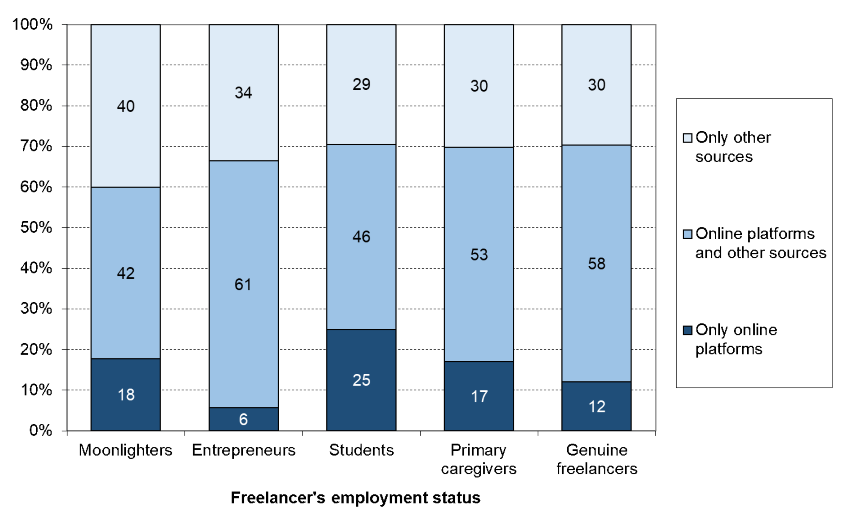

There were also differences in the channels used to obtain jobs depending on the individual’s employment status. Entrepreneurs and genuine freelancers were less likely to use online platforms exclusively (6 per cent and 12 per cent respectively) (see figure 4.13). Instead, they relied on a variety of sources of work, most likely because entrepreneurs and genuine freelancers are more active in the remote work market than other freelancers and therefore have the widest networks of clients and greatest range of opportunities for obtaining work.

Figure 4.13. Channels for obtaining job projects by freelancer’s employment status, 2019 (percentage)

Promises and challenges

5.1. Advantages and disadvantages of freelancing

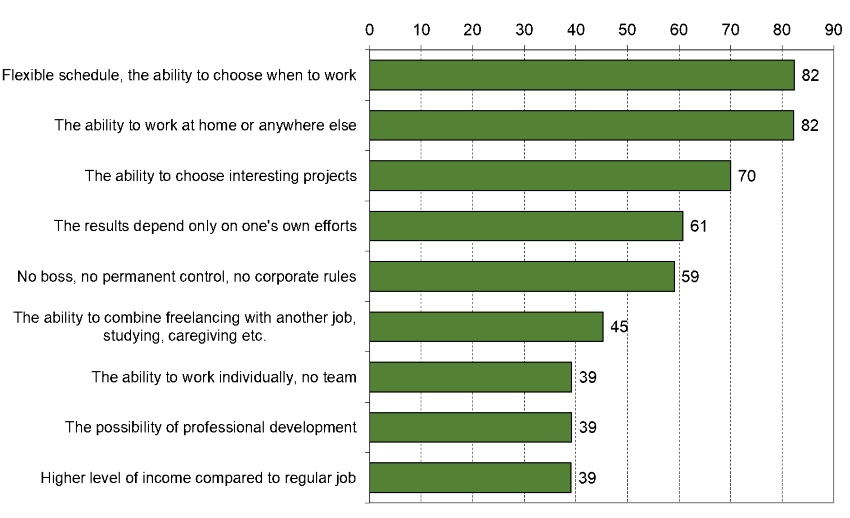

Controversy exists regarding the opportunities and risks of freelance platform work. In our study, when asked about the advantages of freelancing, respondents primarily pointed to the flexible schedule (82 per cent), the ability to work from home (82 per cent), the opportunities to choose interesting projects (70 per cent), personal responsibility (61 per cent) and the absence of any bosses, permanent control and corporate regulations (59 per cent) (see figure 5.1). The main benefit of freelance work, noted by many of the survey respondents, is therefore the freedom to choose when and where they work, with whom they collaborate and which projects and tasks they perform. Freelance work can provide a high level of flexibility for workers. It allows those who prefer to work from home the ability to do so, whether because of health reasons, domestic responsibilities or simply personal preference.

Figure 5.1. Reported personal advantages of being a freelancer, 2019 (percentage)

The reported advantages of freelancing varied depending on the type of employment. Genuine freelancers tended to choose almost all the proposed positive features: the ability to choose one’s working hours (86 per cent), the ability to work from home or elsewhere (84 per cent), the absence of bosses, constant control and corporate rules (66 per cent), the ability to work independently and not as part of a team (43 per cent) and the relatively high level of income compared to working as an employee (44 per cent). For entrepreneurs, the most important features of freelancing were the good opportunities for professional development (52 per cent) and the relatively high level of income compared to working as an employee (58 per cent). Moonlighters and caregivers highlighted the least number of job benefits in comparison with the other types of freelancers; in particular, the absence of bosses, permanent control and corporate rules was much less important for them. They also did not value opportunities for professional development or the higher level of income compared to a regular job. On the other hand, the opportunity to combine freelance work with other types of work was especially important for moonlighters and caregivers, as well as for students (between 69 and 77 per cent).

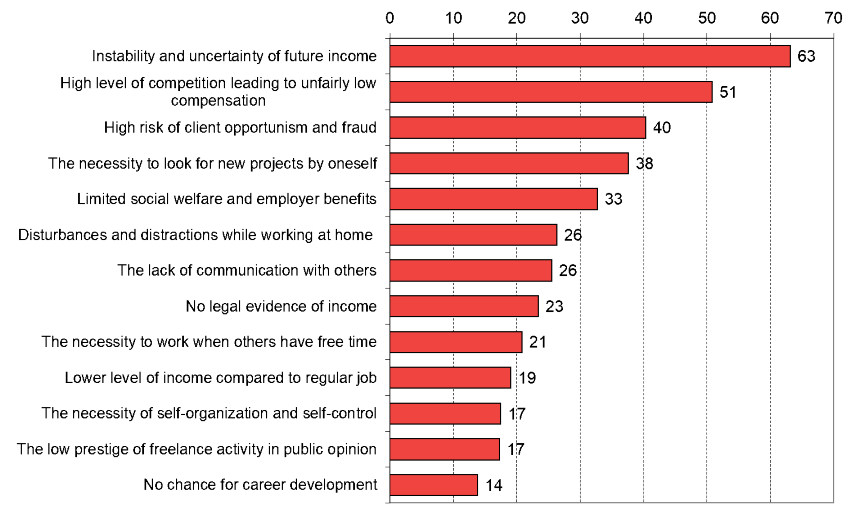

Among all the disadvantages of independent employment for Russian-language freelancers reported over the ten-year study period, instability and uncertainty of future income consistently came in first place (63 per cent in 2019) (see figure 5.2). Other important negative features of freelance work were the high level of competition leading to unfairly low compensation (51 per cent), the high risk of client opportunism and fraud (40 per cent) and the necessity to look for new projects by oneself (38 per cent). Around one third of Russian-speaking freelancers also noted the absence of social welfare and employer benefits. It can be assumed that Russian-speaking freelancers somewhat underestimate the importance of social guarantees in part because of their young age (and, therefore, their lower need for medical services) and the failed pension system (which is not capable of guaranteeing a decent standard of living).

Figure 5.2. Reported personal disadvantages of being a freelancer, 2019 (percentage)

Genuine freelancers were more likely to report the limited social welfare and employer benefits (36 per cent), the lack of communication with other people (30 per cent) and the absence of legal evidence of income (27 per cent) among the disadvantages of freelance work. On the other hand, they were less concerned than other groups about the high level of competition among freelancers, the high risks of client opportunism and fraud and the low chances for career development. Moonlighters were mostly dissatisfied with the lower level of income compared to a regular job. Students and caregivers mentioned the largest number of negative features of freelancing. They were especially worried about the high risk of client opportunism and fraud, the necessity to look for new projects by oneself, the limited social welfare and employer benefits and the low prestige of freelance activity in public opinion. Parallel entrepreneurs, meanwhile, were less likely than any other group to list any disadvantages of freelance work.

The data gathered during the 2019 survey reveal that Russian-language freelancers are quite worried about the probability of not obtaining enough work to maintain their usual standard of living. More than a third (35 per cent) said that they were very worried, and another 32 per cent said that they were rather worried (see figure 5.3). High anxiety was reported most among young and inexperienced freelancers, workers from Ukraine and women freelancers who cared for small children. Conversely, freelancers with a higher level of education and freelance experience, who lived outside of the post-Soviet space, who had professional IT or engineering skills, who worked as moonlighters or parallel entrepreneurs or who worked with regular clients reported being more confident in their future than any other group.

Figure 5.3. Reponses to the question “How worried are you that, in the coming months, you will not be able to get enough projects and tasks to maintain your usual standard of living?”, 2019 (percentage)

5.2. Working hours and work–life balance

Although freelancers can exercise control over their time in ways that are unavailable to standard employees, the reality of self-employment and online platforms places severe constraints on workers’ time and forces them to work long and non-standard hours (Barley and Kunda 2004; Barnes, Green and Hoyos 2015; Osnowitz 2010).

In our study, respondents were asked questions about the number of days and hours that they worked, phrased as follows: “Approximately how many days a week/hours a day do you usually work? Please count not only freelance working hours but also any other forms of paid activity.” Respondents could choose from one to seven days a week and from 1 to 16 hours a day. These figures were then multiplied to produce a continuous variable for the number of working hours per week, which ranged from 1 to 112. In a typical week, freelancers spend an average of 50.2 hours at work. Men work more hours than women (53.3 hours versus 46.1 hours), and moonlighters work the most hours in total (61.8 hours), followed by entrepreneurs (53.6 hours) and genuine freelancers (47.5 hours). As might be expected, students and individuals who care for small children work the least number of hours (37.9 hours and 35.6 hours respectively).

Among freelancers, the share of people working both more and less than the “standard” 40 hours per week is much higher than among the general Russian population (see table 5.1). While more than half (57 per cent) of Russian employees work between 36 and 45 hours a week, only 16 per cent of independent professional work a comparable number of hours. Moreover, one in three freelancers works no more than 35 hours a week, and one in two works more than 45 hours. Furthermore, 28 per cent of freelancers work more than 60 hours a week – more than one and a half times the standard work schedule – which is extremely rare among the general population of Russian workers (8 per cent). One third of freelancers report working every day in some capacity, that is, 7 days per week, and 40 per cent report working ten or more hours per day. It is also noteworthy that the duration of working hours for men is, on average, significantly higher than for women, both among freelancers and among the general working population of the Russian Federation.

Table 5.1. Distribution of non-standard work schedules among Russian-language freelancers in comparison with the general working population of the Russian Federation, 2019 (percentage)

|

|

|

||||||

|---|---|---|---|---|---|---|---|

|

|

|

|

|

|

|

||

|

|

|||||||

|

20 hours or less |

2 |

4 |

3 |

8 |

16 |

12 |

|

|

21–35 hours |

4 |

11 |

7 |

19 |

23 |

21 |

|

|

36–45 hours |

54 |

60 |

57 |

16 |

17 |

16 |

|

|

46–60 hours |

30 |

21 |

25 |

25 |

21 |

23 |

|

|

More than 60 hours |

12 |

5 |

8 |

32 |

23 |

28 |

|

|

|

|||||||

|

Never |

53 |

77 |

65 |

10 |

10 |

10 |

|

|

Several times a year |

13 |

6 |

10 |

22 |

22 |

22 |

|

|

Several times a month |

17 |

9 |

13 |

25 |

28 |

26 |

|

|

A few times a week |

14 |

8 |

11 |

24 |

24 |

24 |

|

|

Almost every day |

2 |

1 |

1 |

20 |

16 |

18 |

|

|

|

|||||||

|

Never |

25 |

42 |

34 |

2 |

3 |

2 |

|

|

Several times a year |

20 |

15 |

18 |

10 |

13 |

11 |

|

|

Once a month |

11 |

9 |

10 |

8 |

9 |

9 |

|

|

Several times a month |

36 |

28 |

32 |

45 |

43 |

44 |

|

|

Almost all weekends and |

8 |

5 |

7 |

35 |

32 |

34 |

Such significant differences in working hours between freelancers and employees leads to differences in the prevalence of non-standard work schedules (see table 5.1). Among freelancers, working non-standard hours is widespread. A third (34 per cent) report that they have to work almost all weekends and holidays, and another 44 per cent work weekends or holidays several times a month, which is also a significant burden on their free time. In addition, 18 per cent of freelancers consistently work at night, and another 24 per cent work after 9 p.m. several days a week. For Russian workers in general, non-standard employment is rather unusual: two thirds never work in the evening or at night (versus 10 per cent among freelancers), and a third never have to perform work duties on weekends or holidays (versus 2 per cent of freelancers).

People who simultaneously encounter both types of non-standard schedules – meaning that they usually work both at night (several times a month or more) and on weekends (once a month or more) – are in the most difficult situation. Among the population of the Russian Federation, only 22 per cent of workers regularly work both at night and on weekends, compared with almost two thirds (64 per cent) of freelancers. Furthermore, while half of all Russian workers (51 per cent) encounter at least one of the two types of non-standard working hours during any given month, almost no freelancers are able to avoid working such hours (91 per cent).

Moreover, although among Russian workers in general men are much more likely than women to work in the evening, at night or on weekends, there is no statistically significant difference between the genders among freelancers; women and men equally bear the burden of flexible employment. The prevalence of non-standard work schedules is extremely weakly associated with other demographic characteristics among freelancers, such as age, marital status, number of children, level of education and employment status. In all groups, approximately 75–80 per cent of respondents reported that they often worked on weekends, and 37–42 per cent of respondents reported that they often worked at night. Only older freelancers (aged 41 and older) were less likely to work at night (32 per cent). Meanwhile, IT specialists (such as programmers and website developers) were more likely to work at night (48 per cent). Our results confirm the conclusions of some qualitative studies, which found that, among freelancers, there were no stable patterns of working time based on socio-demographic characteristics (Donnelly 2011; Evans et al. 2004; Fraser and Gold 2001).

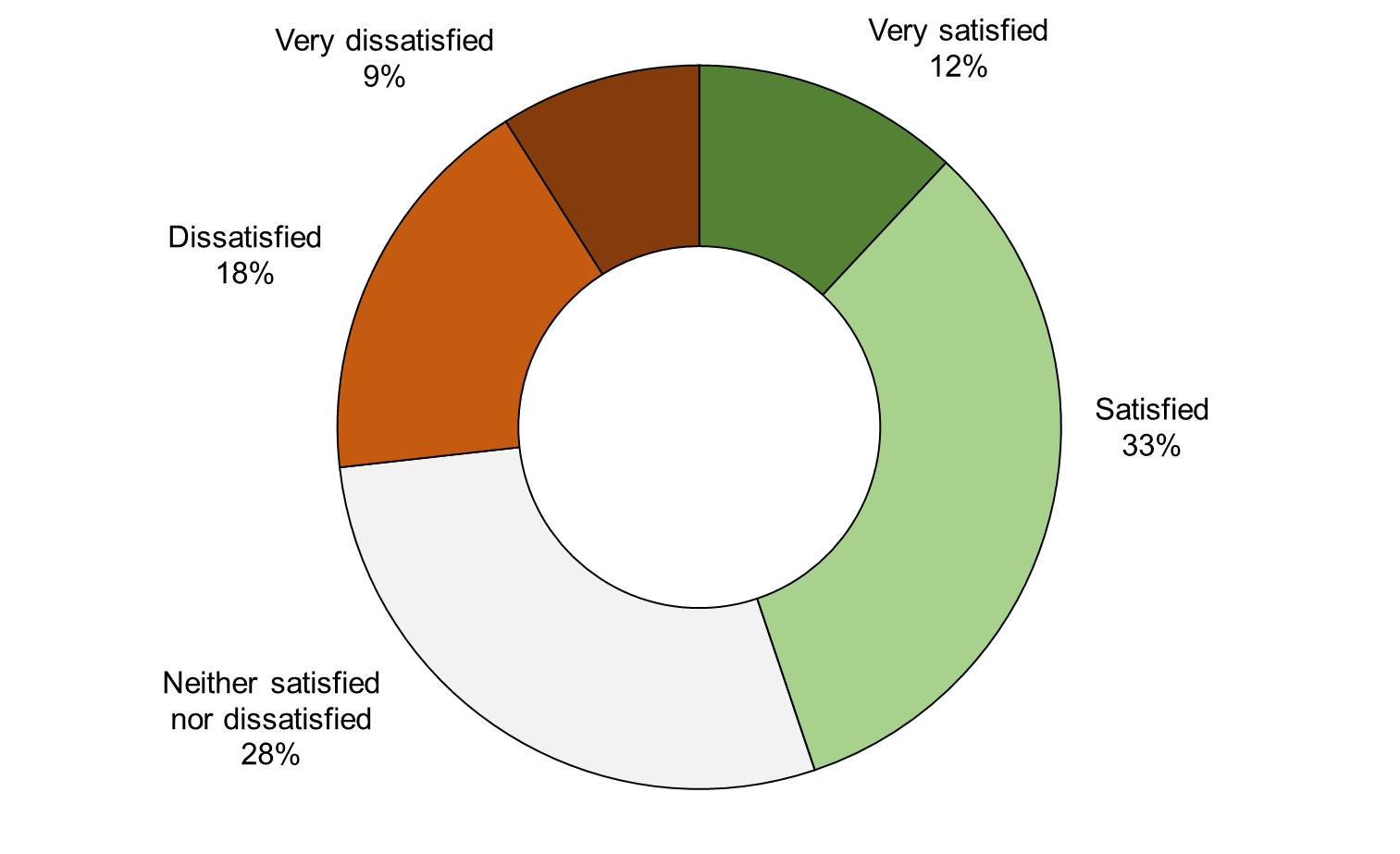

Work–life balance was measured on a five-point scale, ranging from one (very dissatisfied) to five (very satisfied). The question was phrased as follows: “How satisfied are you with the balance between the time you spend on your paid work and the time you spend on other aspects of your life?” In the 2019 survey, almost half of respondents (45 per cent) reported that they were generally satisfied with their work–life balance, and 12 per cent reported being very satisfied. Just over a quarter of freelancers (27 per cent) reported that they were more or less dissatisfied (see figure 5.4).

Figure 5.4. Responses to the question “How satisfied are you with the balance between the time you spend on your paid work and the time you spend on other aspects of your life?”, 2019 (percentage)

The level of emotional exhaustion was assessed through the following question: “Recently, how often have you felt emotionally drained because of your work?” Respondents answered on a five-point Likert scale (1 = never; 2 = rarely; 3 = sometimes; 4 = often; 5 = always). The most popular answers were “rarely” and “sometimes”. Some 70 per cent of freelancers reported that they occasionally felt emotionally drained because of their work (see figure 5.5), while one in four respondents said that they often or always experienced stress and frustration as a result of work.

Figure 5.5. Responses to the question “Recently, how often have you felt emotionally drained because of your work?”, 2019 (percentage)

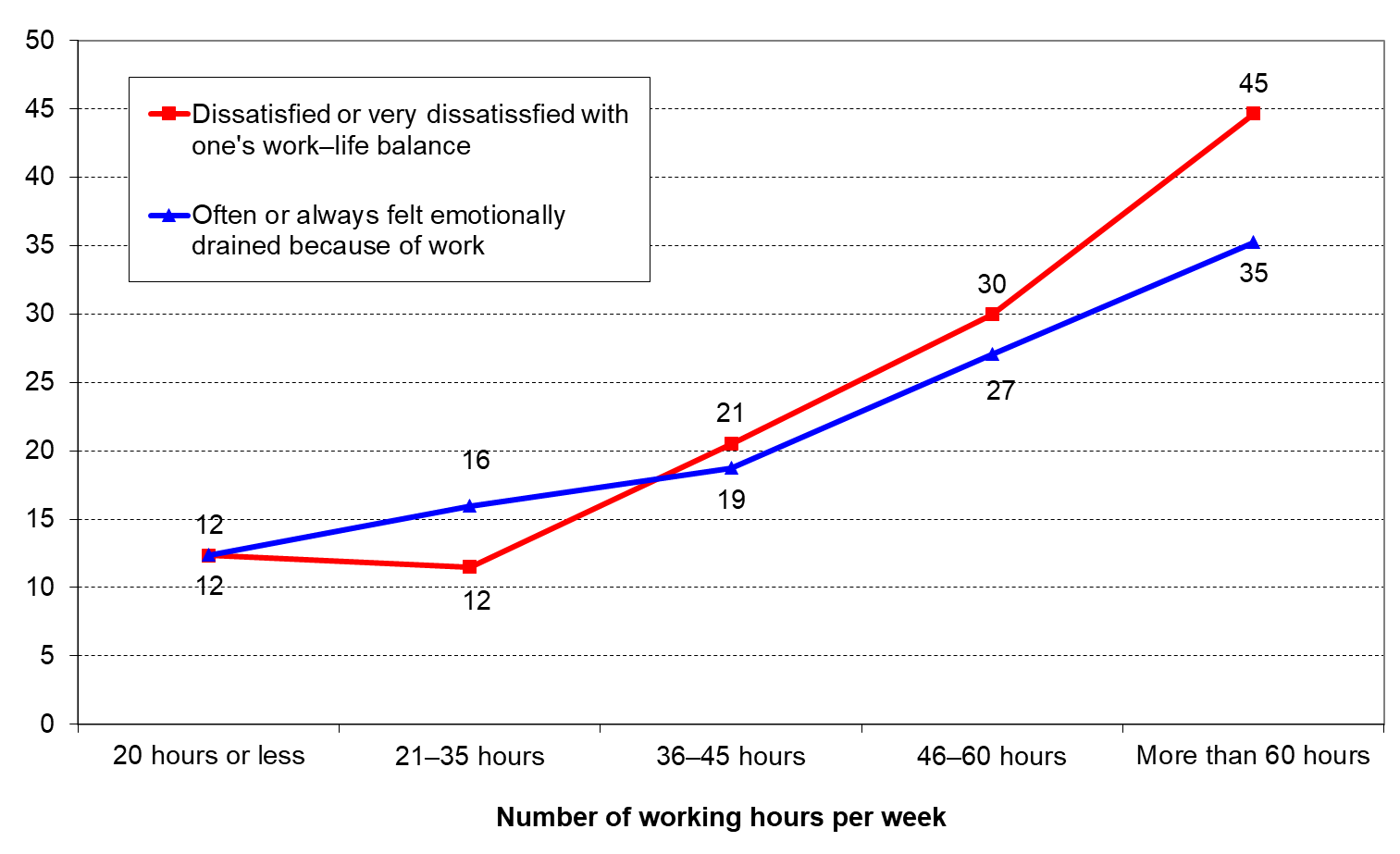

Predictably, and as can be seen in figures 5.6, 5.7 and 5.8, dissatisfaction with one’s work–life balance and emotional exhaustion both increased in line with the rise in the number of working hours, the frequency of working late in the evening and at night and the frequency of working on Saturdays, Sundays and public holidays. Among freelancers who worked 20 hours or less per week, only 12 per cent reported being dissatisfied with their work–life balance or feeling often or always emotionally drained because of their work. Among those who worked more than 60 hours per week, almost half (45 per cent) of respondents were dissatisfied, and more than one third (35 per cent) felt work-related stress, representing a three- to fourfold increase in the level of negative feelings (see figure 5.6). Levels of stress and dissatisfaction were also two to three times higher among freelancers who almost always worked late into the evening, at night and on Saturdays, Sundays and public holidays (29–37 per cent), compared with those who almost never worked such hours (13–18 per cent) (see figures 5.7 and 5.8).

Figure 5.6. Work–life balance dissatisfaction and emotional exhaustion among freelancers by the number of working hours per week, 2019 (percentage)